5 Steps to Planning and Financing Your Construction Project

Home & Land Financing

If you’ve been dreaming of wide-open spaces, fresh air and a home that reflects your rural lifestyle, you’re not alone. Building a home in the country offers endless opportunities, from raising livestock and growing your own food to simply enjoying the peace and quiet of nature. But before you break ground, it’s important to understand the steps involved in planning and financing your construction project. At Farm Credit of the Virginias, we specialize in helping rural homeowners bring their vision to life. Here’s a five-step guide to help you get started:

1. Choose the Right Location

It’s the most important factor whenever you buy real estate. Consider what your needs are now and what they will be 10 years from now. As your family grows, will the location help or hinder your family’s ability to enjoy the property? If you choose a rural location, how much infrastructure might you require to meet your needs (access to major interstates, schools, shopping, healthcare, etc.)?

Other location factors to consider when choosing a home site:

- Available amenities: Consider availability and cost to add required utilities such as sewer/septic, gas, well, water, etc.

- Perc test results: If you intend to use a septic system, the soil at the home site must have a suitable absorption rate to support a septic system.

- Special assessments: Be aware of charges levied against certain home sites, such as installation of water or sewer lines, street lighting, police and fire protection, or other special services.

- Zoning limitations: Research zoning restrictions on minimum setbacks, limits on size or existence of accessory buildings, home size or usage.

- Noise concerns: Identify any source of potentially undesirable noise, such as a train track, busy freeway, concert venue, fire department, etc.

- Surveys: If you’re not sure about the property’s boundaries or access, spend the money for a survey. It’s the only way to be sure of exactly what you own.

- Flood zone: Is the property in a flood zone? If so, you will need to figure out whether or not flood insurance is mandatory and how much that will cost.

2. Plan Your Build

Once you’ve found the ideal site for your future home, the next step is planning the construction.

Choose a reputable builder.

There are many options for home construction and many different builders. Some builders offer turnkey contracts, while others offer contracts that are more open to interpretation. Contracts that don’t address all aspects of construction can create additional costs and headaches during construction, especially if some items weren’t considered upfront.

Ask the following questions:

- How many years have you been in business?

- Are you a licensed contractor?

- May I see a copy of your insurance certificate?

- How long do you expect the construction process to take?

- How many different jobs do you typically work on at the same time?

- Who will be responsible for securing the required permits?

- Who will be in charge of clean up at the end of each day?

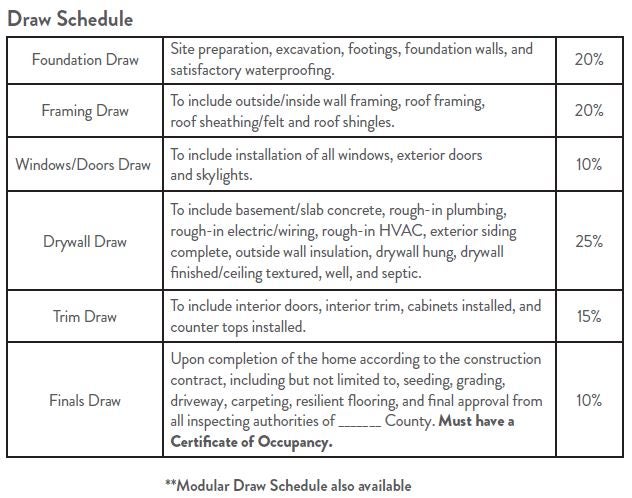

- How do you typically structure your draw schedule?

- How do you handle any construction contract changes?

- What is included in the base cost of my construction contract? What is considered an upgrade?

- Can you share references with me? Can I tour a few of your completed homes?

Think about cost overruns.

Unfortunately, when it comes to constructing a home, things don’t always go as planned. What happens if the excavator hits more rock than expected? What if you change your mind about the kitchen layout or decide you want to upgrade your countertops after construction has already started? Those possibilities and more speak to the importance of setting some money

aside for unanticipated issues.

A lender looking out for your best interest may possibly increase your loan amount as a cushion to cover unpredicted costs or verify that you have additional funds available if needed. A good overrun rule of thumb is adding 7-10% of the anticipated cost of construction. Planning for overruns helps the construction process continue even when the unexpected happens.

3. Secure Financing

After selecting your contractor, the next step is securing financing for your project.

What can you afford?

When considering your construction budget, ask yourself the following questions:

- What is the most you would be comfortable with as your monthly payment?

- If applicable, do you have the cash reserves to make two house payments?

Back-End Ratio

The back-end ratio, also known as the debt-to-income ratio, indicates what portion of your monthly income goes toward paying debts. Total monthly debt includes expenses, such as mortgage payments (principal, interest, taxes and insurance), credit card payments, child support and other loan payments. It does not include living expenses such as monthly utility bills, groceries or travel.

Back-End Ratio = (total monthly debt expense gross monthly income) x 100

Example: Borrower with monthly income of $5,000 ($60,000 annually 12) and total monthly debt payments of $2,000. This borrower’s back-end ratio, then, is 40% ($2,000 $5,000 = 0.4 x 100 = 40%).

Back-end ratio standards and guidelines vary. Farm Credit of the Virginias typically recommends that the ideal back-end ratio should be 45% or lower. Depending on your credit score, savings and down payment, your lender may accept a higher back-end ratio.

Be prepared to provide:

Personal Information

- Signed, completed application

- Borrower’s Authorization Form to release information

- Valid photo identification

- Income verification

» Pay stubs for a one month period within 60 days of application

» W-2s or Federal Tax Returns for the last two years

» Self-employment or commission-based jobs may require additional documentation

» Verification of significant assets for funds needed to cover closing costs or debts not on your credit report

Property Information

- Final signed construction contract, including building plans and specifications

- Legal description of property

- Survey (if applicable)

- Name, address and phone number of seller or land contract holder

- Copy of signed sales agreement (if purchasing land or if land is not already owned)

4. Complete an Appraisal

An appraisal is required prior to loan closing to ensure the completed home is worth the value of the loan. Appraisals are standard practice for lenders to ensure the value of the loan’s collateral (in this case, your new home). Farm Credit of the Virginias will order an appraisal to estimate the future value of the home once the project blueprints and building specs are finalized.

Items Needed for Appraisal

- Final signed construction contract

- Dwelling specifications – provides the intricate details of the home construction

- Property information – legal description, survey and/or deed

- Complete plans – front, rear and side elevations

5. Close and Begin Construction

After credit review and approval of both appraisal and title work, Farm Credit of the Virginias will schedule a closing date. You will need to provide evidence of Builder’s Risk Insurance to cover the construction period prior to closing. Insurance protects you against theft, fire, weather damage or vandalism of materials on your property.

After closing, Farm Credit of the Virginias will help manage disbursements with your contractor and perform on-site inspections as needed. Fast disbursements and personal knowledge of the project help ensure construction is completed on time.

Ready to Build?

Whether you’re planning a stick-built, modular or log home, Farm Credit of the Virginias offers flexible financing with no acreage limits, interest-only construction periods and competitive long-term rates. We’re here to help you build the rural lifestyle you’ve always dreamed of. Reach out to a Farm Credit loan officer at 1 (800) 919-3276 or contact us online to get started!