Preparing For 2024: Recommendations For Your Household, Farm & Business

Farm Management Resources

Financial Literacy

Is it just me, or does time move a lot faster these days? I just blinked, and 2024 is almost here. That means it’s time for Doc White’s thoughts on how you should start preparing for the new year. Before I get to my recommended actions, let’s look ahead and see what 2024 might have in store for us.

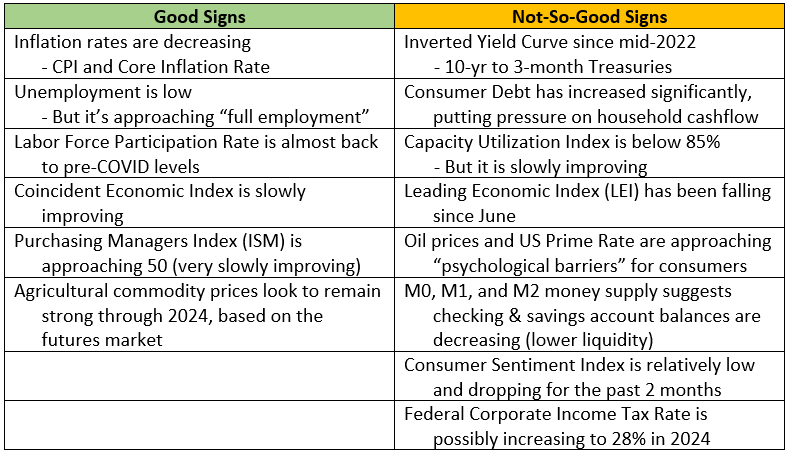

I’ve been in several meetings recently that have discussed the economic outlook for the next twelve months. Needless to say, it’s a murky picture – unrest in Gaza, war in Ukraine, election season in the US, and an on-again/off-again COVID situation are throwing economic models into chaos. I’m not a market economist with fancy models – so here’s my Jethro Bodine-level macroeconomic interpretation of the most recent US economic indicators:

Boiling down this information, I’m expecting a downturn in the overall US economy over the next 9-12 months for households and general business. However, I’m relatively bullish on agricultural commodity prices for the next year or so. That said, here are my recommendations to help you prepare for 2024:

Recommendations For Your Household:

- Build your liquidity to have more of a cushion should the economy head south. Beef up your savings account and/or pay down your high-interest consumer debts by cutting your household expenses.

- Tighten up your household spending budget. Inflation will probably be sticky – prices may be slow to decrease, if they do at all. Higher interest rates and higher oil/energy prices may lead to higher food prices at the grocery store and gas stations. Look for ways to reduce your discretionary expenses.

- Update your estate planning documents to reflect any changes in regulations or your lifestyle. Revise your wills, powers of attorney, advance medical directives, and other documents due to changes in your family & financial condition. Make an appointment to meet with your attorney and estate planning team.

- Update the beneficiaries on your insurance policies and retirement accounts to reflect changes in your life. Schedule a meeting with your insurance agents and financial professionals.

- Review and revise the diversification of your retirement investments (IRAs, 401(k), etc.). A well-diversified portfolio can reduce the risk during an economic unstable period.

- Continue to make regular monthly or quarterly investments into your retirement investments if the economy stalls. Dollar-cost averaging is an investment strategy that helps you reduce the average cost of your investments. A downward-trending economy is actually a good time to invest – you can invest in stocks that are “on sale”, so your regular monthly investment will purchase more shares!

Recommendations For Your Farm & Business:

- Talk with your accountant and financial advisors about possible reactions to the proposed increase in the federal corporate income tax. The budget for 2024 proposes increasing the corporate tax rates from 21% to 28%. Should you consider becoming a “pass-through” entity to reduce your effective income tax rate? Work with a qualified tax professional to develop your long-term tax plan.

- Give your operation a “Financial Wellness Exam”. Determine your current status and identify possible areas of concern. Work with your lender and accountant to analyze the liquidity, solvency, repayment ability, profitability, and financial efficiency of your operation.

- This will help you make those year-end decisions about tax moves. Maybe you are better off using your profits to build your liquidity or pay down your loans rather than purchasing assets you don’t need just for the sake of reducing your taxes. Remember, you need to spend roughly $5 to save $1 in income taxes – that can severely hurt your cash flow if you aren’t careful. Knee-jerk tax moves can hamstring your operation.

- Review and revise your written business plan for the upcoming year. Have your business goals changed? Have there been significant changes in your operation that need to be updated? A business plan is your guidebook to the business’ future. Remember, it’s not a once-and-done activity. Your business plan needs to grow and change as your business changes. If you do not have a written business plan, consider enrolling in the Farm Credit Knowledge Center’s AgBiz Planner program to get help developing a plan for your farm.

- Schedule time before year-end to talk about the transition plan for your operation. Review and revise your existing transition plan to account for major life events or changes in your goals. Take time to plan for the transition of your operation so that you don’t put your family, business partners, and employees behind the eight ball should something happen to you. Get a copy of Farm Credit University’s Family Business Transition Workbook to start the process if you haven’t already!

- It wouldn’t be a Doc White blog if it doesn’t mention retirement planning. Talk with your financial team about the potential benefits of starting a SIMPLE-IRA, SEP-IRA, or a Solo 401(k)-type plan for your operation. It’s a way to recruit/retain good employees and protect your net worth, as well as a way to get great tax benefits! Your contributions are tax deductible for the business AND the funds grow tax deferred as long as they are in the IRA. You can reduce your income taxes by writing a check to yourself.

- Talk with your financial team about the possibility of leasing certain assets instead of purchasing them. Consider the impact on your cash flow, management flexibility, and income taxes. For some assets, leasing be a better long-term option for your farm.

- Finally, schedule a business meeting before year-end. I find that farm/business owners get so busy that they don’t take time to plan for the future of the operation. Schedule time for planning, otherwise it happens on the fly – and that may not be in your best interest. Put together an agenda of the key planning issues that you need to think through. Invite someone who can help you improve the management of some aspect of your operation. Keep written minutes of your meeting, especially if you are an LLC, S-corporation, or C-corporation – this might also help preserve your limited liability in the case of a lawsuit.

Author:

Dr. Alex White

Virginia Tech, Dairy Science at the School of Animal Sciences