What is the Loan Application Process?

Financial Literacy

As a loan officer, one question that I help answer on a daily basis is, “I’m new to Farm Credit. What do I need to do to apply for a loan?”

What seems like a fairly straightforward question can be interpreted in many different ways and have more than one answer. The biggest thing to keep in mind is that no two loan requests are ever quite the same. It is a lender's responsibility to provide the necessary support and guidance to make the loan process as seamless as possible.

Most initial loan requests fall into two categories:

- The applicant knows what they want to purchase (i.e., a specific piece of real estate, # of head of beef cattle, new tractor, etc.). This borrower already has the estimated purchase price of the asset and is ready to make an application and start the official loan process.

- The applicant is considering buying something (in the very early stages). This could be a variety of things. For example, purchasing real estate, a new piece of equipment, breeding livestock, or even a construction request. They are unsure of the purchase price and may not exactly know what they are looking for yet. What they do know is that they want to purchase something and will possibly need a loan to assist them. These types of requests fall into our “Pre-Qualification”

The Conversation with Your Lender

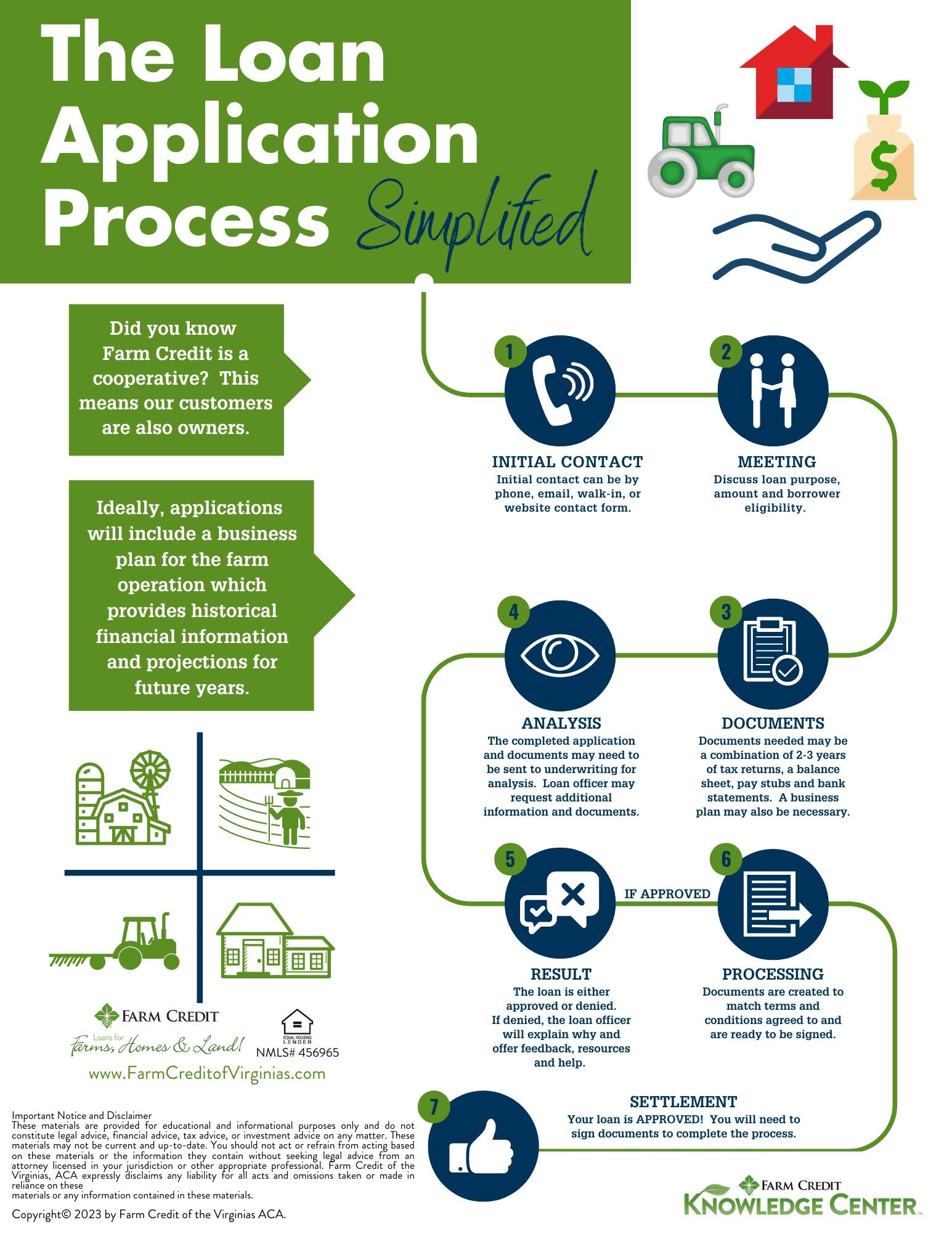

Even though these two requests are very different, they both most likely started the same way- with a conversation. This is the initial step in the loan process. During that conversation, a lender will ask the inquiring individual many questions to determine what they are purchasing, their plans, and if there is a loan product that fits their need.

Documents Gathered and Reviewed

If/when the applicant is ready to move forward, the first thing that a lender will require is a completed application and copies of all applicant IDs. Other items that may be requested include a variety of financial documents including but not limited to:

- Personal Tax returns (typically three years)

- Business Tax Returns, if applicable (typically three years)

- Most recent W-2 or 1099 for all applicants

- Personal Balance Sheet

- Verification of assets- most recent statements for any bank accounts, investment accounts, retirement accounts, etc.

- Most recent pay stub for all applicants

- Signed contract or bill of sale

**Additional items may be requested depending on the nature and complexity of the request. A lender will communicate with you to determine what those may be.**

This is a great time for the lender and applicant to set up an appointment and go over the specific items needed and any forms that will have to be completed. A Credit Application, in particular, is a document that can initially be overwhelming, especially for a first-time borrower. The lender will be able to guide the applicant through the various parts of the form, including the balance sheet, and provide clarity to any questions pertaining to the application or other documentation that may have been requested.

Loan Application Submitted for Processing and Credit Review

Once an application has been completed, IDs and the requested financial items are received, the official loan process will begin. A lender will submit the loan request to a Processing Center. The processor will pull the applicant's credit score and communicate that report to the loan officer. The application is then further reviewed for analysis. This process may be completed by the lender, or the request may be sent to a credit underwriter for their review. At this point in time, a loan officer will be in constant communication with both the applicant and the underwriter assigned to the request. All parties will work together to ensure that the appropriate documentation is received and provide answers to any questions regarding the request. From there, a decision will be provided. If approval is granted, the next steps and what is needed to proceed with the request will be discussed. If the request is denied, the lender will explain how they came to that decision and provide guidance and help answering any questions or concerns.

Pre-Qualification Requests

For requests that fall into the pre-qualification category, a similar evaluation process is completed. The lender will review your loan application and determine if a pre-qualification can be granted or if the request will need to be denied. If the pre-qualification is provided, the loan officer will continue to follow up with the borrower to determine if/when they are ready to proceed with the official loan application. At that point in time, your lender will be able to discuss with you what information is required and what will be needed before formal approval can be granted.

Loan Approval – Getting Closer!

If the loan is approved, the applicant and lender will discuss the loan terms, rates, fees, and any necessary conditions that are required as part of the formal approval of the loan. From there, the request will move on to loan processing. The loan processor assigned will prepare all the essential loan documents, ensuring that all loan conditions and terms are included in the paperwork. Depending on what the loan is for will determine what further steps will need to be completed prior to loan settlement and funding. For example, if the request is for the purchase of real estate, the loan officer will order an appraisal on the property that will be used as collateral for the request. In addition, the loan officer will need to ensure that the property has no liens placed against it. They will coordinate with an attorney or Title Company and ask them to complete a standard title search on the property, confirming that the property is “free and clear” of all liens and encumbrances. The lender will continue to be the main point of contact during this time. They will let the applicant know what items may be pending and where they are in the loan process.

Loan Closing – You’re There!

When all loan conditions and terms of approval have been met, a settlement date will be set. At this point in time, the applicant will sign the loan documents, and the loan will be funded. The loan process is complete!

Download the Loan Application Process infographic.

Author

Elsa Southard

Loan Officer, Farm Credit of the Virginias